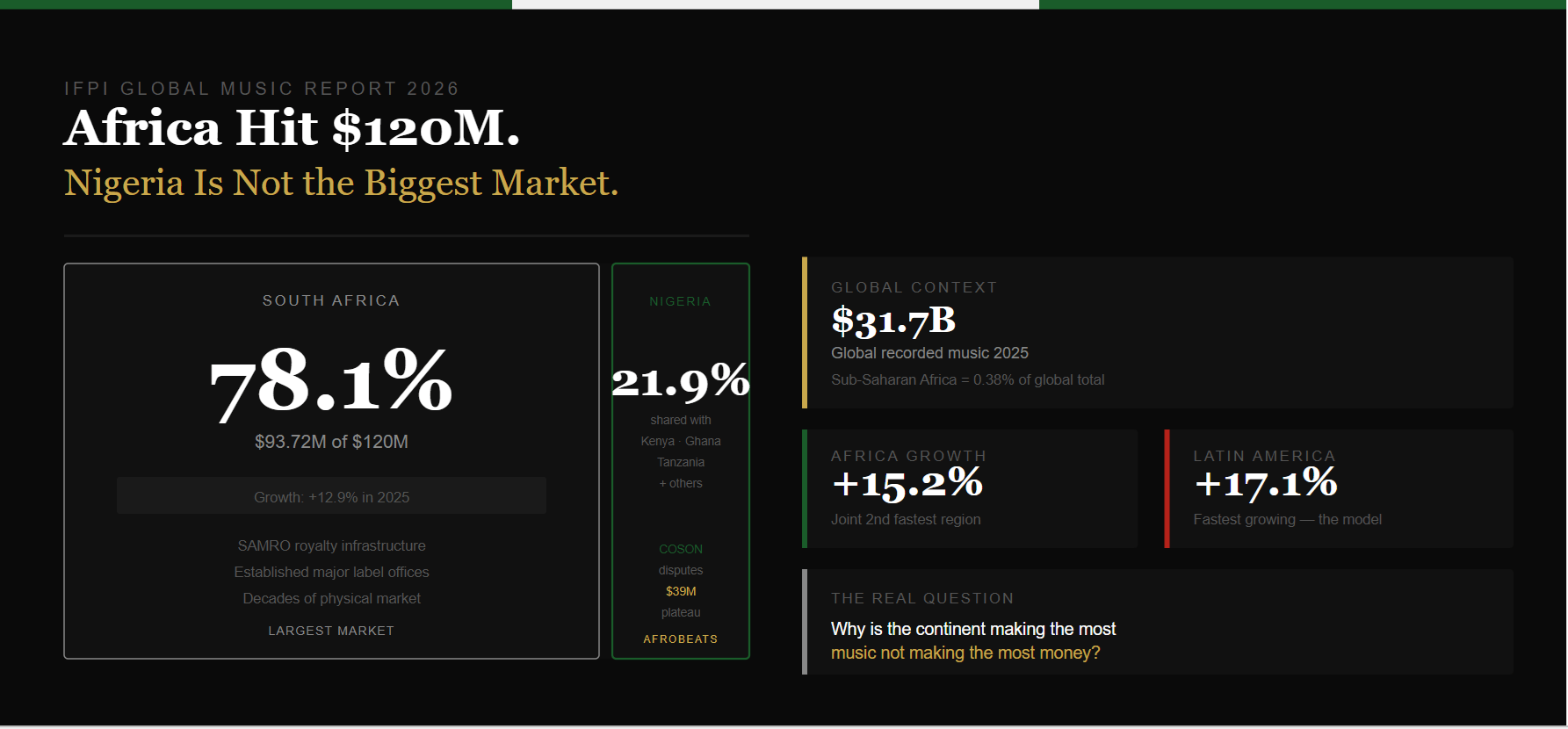

African Music Hit $120 Million in 2026, Nigeria Is Not the Biggest Market

The headline number that came out of the IFPI Global Music Report 2026 last week was $31.7 billion: global recorded music revenues hitting an all-time high for the eleventh consecutive year. Every region grew, including Africa music revenue. Streaming is still the engine 837 million paid subscribers worldwide.

Nigerian music publications ran the Africa angle. Sub-Saharan Africa grew 15.2%. $120 million. Good news. Strong trajectory. Everyone moved on. Nobody ran the number that actually matters for Nigeria.

South Africa took 78.1% of that $120 million. That is $93.72 million going to one country. Nigeria, the country whose Afrobeats artists are filling arenas in London and headlining Coachella, is competing for the remaining 21.9% of a $120 million regional pie alongside Kenya, Ghana, Tanzania, Senegal and every other Sub-Saharan market. The country making the most culturally significant music on the continent is not the country making the most money from it. That is the story.

Africa Music Revenue: What the IFPI Report Actually Shows for Africa

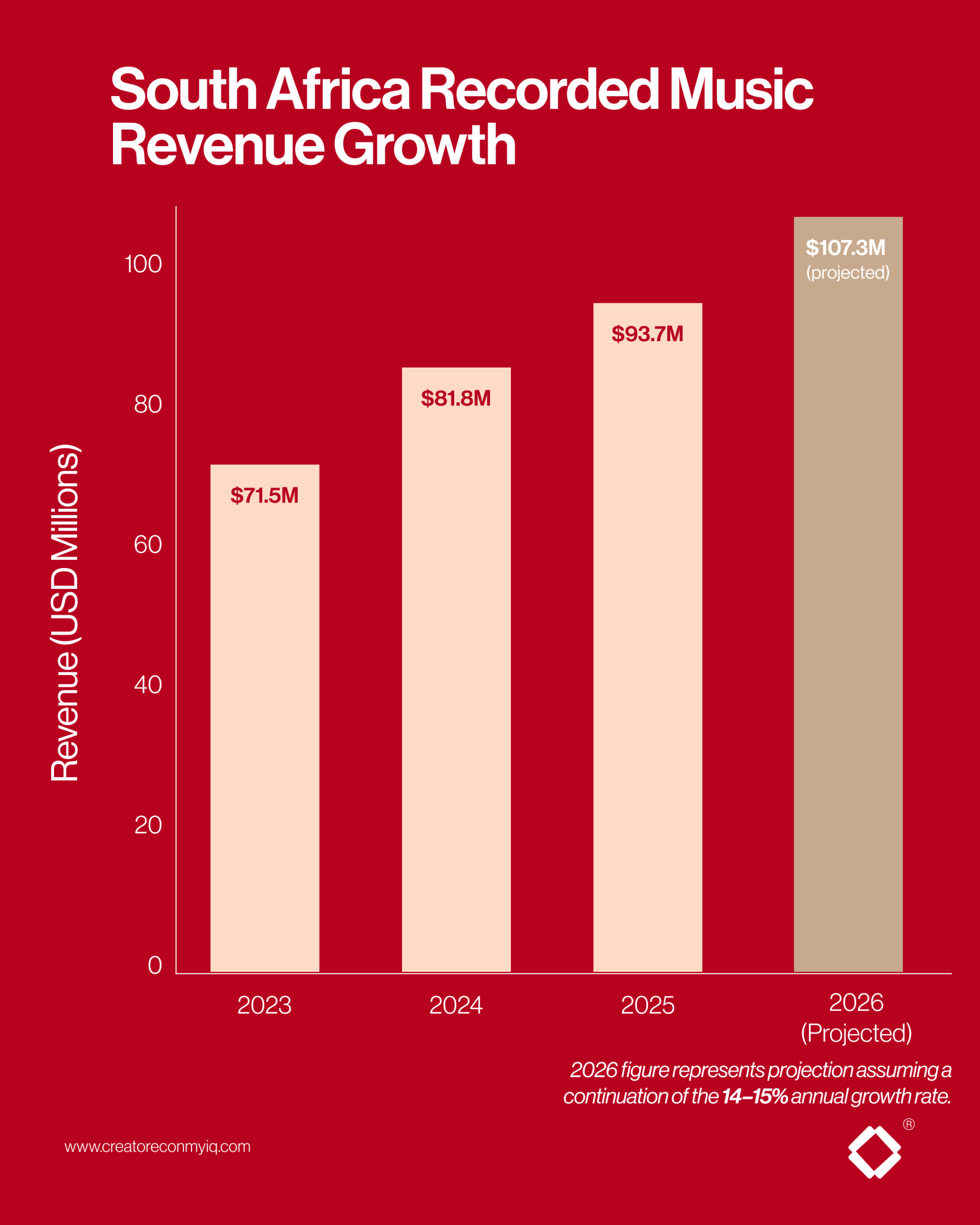

Sub-Saharan Africa saw recorded music revenue growth of 15.2% in 2025, reaching $120 million. South Africa remained the largest market in the region and accounted for 78.1% of revenues following growth of 12.9%.

To put those numbers in context: global recorded music revenues hit an all-time high of $31.7 billion in 2025, marking the eleventh consecutive year of growth. Sub-Saharan Africa’s $120 million represents 0.38% of global revenues. A region of over one billion people, home to some of the most streamed music on the planet, capturing 0.38% of the industry’s total value.

Angela Ndambuki, IFPI regional director for Sub-Saharan Africa, described the growth as reflecting a “sustained and powerful upward trajectory” driven by record company investment, the growing global influence of African artists, and increasing adoption of licensed streaming services.

That framing is accurate. The growth is real. However, 15.2% growth on a small base is still a small number. And South Africa’s structural dominance of that base means Nigeria’s position is weaker than the headline suggests.

The South Africa Problem

South Africa taking 78.1% of Sub-Saharan Africa’s recorded music revenues reflects decades of infrastructure investment a functioning royalty collection society in SAMRO, established major label offices, a domestic music industry that monetised through physical sales long before streaming arrived, and an economy with higher per capita income and more stable currency than most of its regional neighbours.

South Africa built the infrastructure and it is paying off. The question is why Nigeria, which has been producing more globally consumed music than South Africa for the past decade, has not built comparable infrastructure for capturing the financial value of that music domestically.

The answer connects directly to everything else happening in Nigerian music right now. Wizkid, Davido, Burna Boy, Tems and Rema generate enormous streaming numbers, but the royalty infrastructure to capture that value efficiently within Nigeria is still underdeveloped. The Copyright Society of Nigeria, called COSON, has faced years of governance disputes and operational challenges that have limited its effectiveness as a royalty collection body. Performance rights revenues, the money artists earn when their music is played in venues, on radio and in public spaces leak out of the Nigerian system at a rate that would not happen in a market with functioning collection infrastructure.

IFPI‘s Ndambuki noted that addressing challenges such as streaming fraud and gaps in monetisation will be critical to ensuring that growth translates into lasting benefits for creators across the region. The monetisation gaps she is referring to are particularly acute in Nigeria.

What the Global Numbers Tell You

Paid subscription streaming revenues increased 8.8% and accounted for more than half of global revenues at 52.4%. There are now 837 million users of paid streaming subscription accounts globally.

That 837 million figure is the one that should concern Nigerian music industry stakeholders. The global streaming subscriber base is enormous and growing. Nigeria’s contribution to that subscriber base paying users on Spotify, Apple Music, Tidal and other platforms is still relatively small. Most Nigerian music consumption happens on free tiers, on YouTube, on Audiomack‘s free service, or through informal channels entirely.

A listener on a free tier generates advertising revenue. Ad-supported streaming grew 4.3% in 2025 compared to subscription streaming’s 8.8%, and the per-stream rate is significantly lower. Nigerian artists are accumulating billions of streams but a disproportionate share of those streams are generating the lower-value advertising revenue rather than the higher-value subscription revenue.

Artists’ share of industry revenues increased slightly from 34.8% in 2024 to 35.5% in 2025, and has grown significantly over the last decade from 31% in 2016. Artists globally are getting a slightly larger piece of a growing pie. Nigerian artists are getting a slightly larger piece of a much smaller slice.

The Streaming Fraud Problem Nobody Is Talking About in Nigeria

IFPI CEO Victoria Oakley said streaming fraud is theft, plain and simple, and called on organisations with the scale and data to act decisively.

In January 2026, Deezer reported receiving more than 60,000 fully AI-generated tracks every day, with 85% of streams on AI-generated music across the platform in 2025 being fraudulent up 70% from the previous year.

This matters for Nigerian artists specifically because streaming fraud artificially inflated play counts using bots, fake accounts and AI-generated content, siphons royalty pool money away from legitimate artists. When the total royalty pool for a given period is divided among all streams, fraudulent streams reduce the per-stream rate for genuine music. Nigerian artists who are already generating lower-value streams from a market with low subscription penetration are further disadvantaged when fraud inflates the denominator.

The problem is not unique to Nigeria but the structural vulnerability is higher here than in markets with better-developed monitoring infrastructure.

Latin America Is the Model Nigeria Should Study

Latin America was the fastest-growing region at 17.1% year-on-year. It also consistently produces globally consumed music reggaeton, Latin pop, Brazilian funk from countries with economies that share some characteristics with Nigeria’s emerging market profile.

What Latin America has built that Nigeria has not is functioning domestic royalty infrastructure, active streaming subscription growth in local markets, and partnership models between international labels and domestic artists that capture value locally rather than exporting it entirely to Western label structures.

Bad Bunny, J Balvin, Karol G and Peso Pluma generate enormous streaming revenues. Universal Music, Sony Music and local label structures in those markets capture a meaningful portion of that value flows back into Latin American music economies in ways that Nigerian music economics currently do not replicate. The comparison is not perfect but the direction of travel is instructive.

What $120 Million Actually Means for Nigeria

If Nigeria captured its proportional share of Sub-Saharan Africa’s music revenues , based on its cultural output and global streaming presence , it would be the region’s largest market, not South Africa. The fact that it is not tells you everything about the gap between cultural impact and commercial infrastructure.

The $39 million plateau in Spotify earnings we wrote about last week fits inside this larger picture. Nigeria’s recorded music revenues across all formats , streaming, physical, performance rights, synchronisation , are constrained by the same structural weaknesses. Collection infrastructure. Currency volatility. Low domestic subscription penetration. Governance challenges at royalty bodies. Dependence on international label structures that capture value abroad.

IFPI’s report offers the definitive snapshot of an industry that continues to grow while adapting to profound technological and cultural change. For Nigeria, adapting to that change means building the infrastructure to convert cultural dominance into financial dominance. The gap between those two things is currently very wide.

African music hit $120 million in 2025. Nigeria is not the biggest beneficiary of that growth. That is not inevitable. It is a policy and infrastructure problem. And it is one the Nigerian music industry is running out of time to solve while its artists are still at the height of their global influence.