On March 5, 2026, Canal+ confirmed what the Nigerian film industry had been whispering about for months. Showmax was dead off the Nollywood streaming economy.

Eleven years. Over $428 million in accumulated losses. A $309 million relaunch backed by NBCUniversal Peacock technology. Forty-four African countries. Hundreds of commissioned originals. In the end, Canal+ CEO Maxime Saada told investors the platform was simply not commercially successful and shut it down nine weeks after the announcement.

Less than nine months before that, in June 2025, IROKOtv officially closed after 15 years of operation. Jason Njoku had built it from scratch, attracted Tiger Global as an investor, raised $35 million in venture capital and spent over $100 million in combined funding trying to win the Nigerian streaming market. He reflected afterward that they could have reached the same conclusions with $5 to $10 million. Streaming was not the winning model for Nollywood in Nigeria.

Netflix had already confirmed in November 2024 that it would no longer commission Nigerian content, shifting instead to licensing deals. Amazon Prime had pulled back from African originals earlier that same year.

Within twelve months, every major subscription streaming platform with meaningful Nollywood ambitions had either retreated or collapsed entirely. The Nigerian film industry should be in crisis. It is not. And the reason why tells you something important about where the real money in Nollywood has always been.

The Nollywood Streaming Numbers That Explain Everything

While Showmax was burning through hundreds of millions of dollars chasing Nigerian subscribers who were not coming, something else was happening on a platform nobody was treating as a competitor to Netflix.

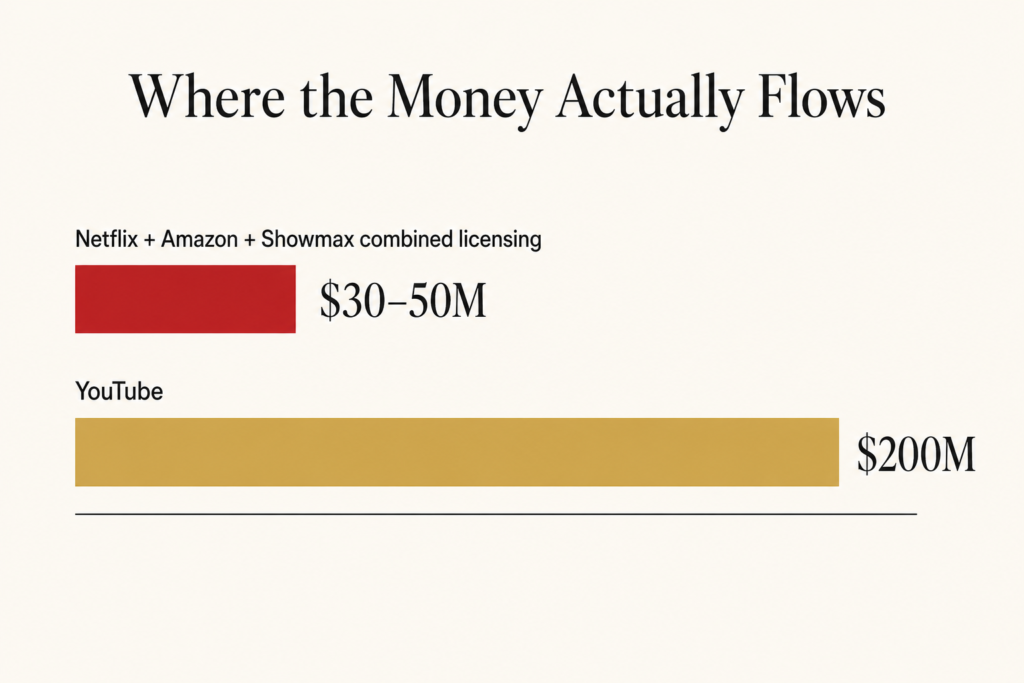

Nollywood-focused YouTube channels collectively generated an estimated $10 to $15 million per month in 2024. Annually that approaches $200 million, four times what Netflix, Amazon and Showmax combined paid Nollywood in licensing fees over the same period.

The comparison is stark. The subscription model that received the most investment, the most press coverage and the most industry attention generated $30 to $50 million annually for Nigerian filmmakers. YouTube, which required no investment from platforms, no commissioning deals, no licensing negotiations, quietly generated four times that figure through advertising revenue on free content.

Nigeria has 31.6 million YouTube users. Netflix has 169,000 subscribers. That ratio is not a market failure. It is a market signal that was available to anyone paying attention.

The structural reason is simple once you follow it. A $5 monthly subscription might seem trivial in London or New York. In Nigeria, where GDP per capita hovers around $2,000, that same $5 represents a meaningful portion of a household’s daily food budget. A global study found that seven of the ten countries where people work the longest to afford a Netflix subscription are in Africa. The subscription model was designed for economies with fundamentally different conditions. Importing it into African markets without adaptation has proven, repeatedly, to be catastrophic.

YouTube removed the affordability barrier entirely. You do not need a credit card. You do not need a subscription. You watch, the ad plays, the creator earns. That model is perfectly aligned with Nigerian economic reality. The platforms that built around it, IrokoTV in its early ad-supported experiments and Nollywood producers uploading directly, understood something that Showmax’s $428 million never figured out.

What Nollywood Actually Built on YouTube

The specific numbers behind the YouTube Nollywood economy are worth examining because they reveal an industry that has been quietly building sustainable infrastructure while the subscription drama played out.

Up to 40 percent of ad revenue from Nollywood YouTube channels comes from diaspora audiences in the US, UK and Canada — viewers whose advertising rates are significantly higher than Nigerian domestic rates. A film that pulls 20 million views in Nigeria generates meaningful income. The same film pulling additional millions from London and Houston generates premium advertising revenue that compounds the returns.

Omoni Oboli’s Love in Every Word racked up over 20 million views in just three months. Films like Last Straw, The Homecoming and Broken Hallelujah regularly hit the 10 million views mark. Unlike cinema releases or streaming exclusives which generate revenue once, YouTube allows films to earn for years after upload. A film released in 2022 is still generating advertising revenue in 2026 every time someone watches it.

That long-tail model is structurally more aligned with how Nollywood actually produces content than any subscription platform model was. Nollywood produces over 2,500 films annually — the second-largest film industry globally by volume. The subscription model could never absorb that volume. Its commissioning budgets were too limited, its quality filters too narrow, and its preference for internationally palatable narratives too restrictive for an industry built on prolific, audience-specific storytelling.

YouTube absorbed all of it. And paid for all of it.

What the Theatrical Surge Tells You About Nollywood Streaming

The most counterintuitive data point in the current Nollywood business picture is what happened at the cinema box office at exactly the same time streaming was retreating.

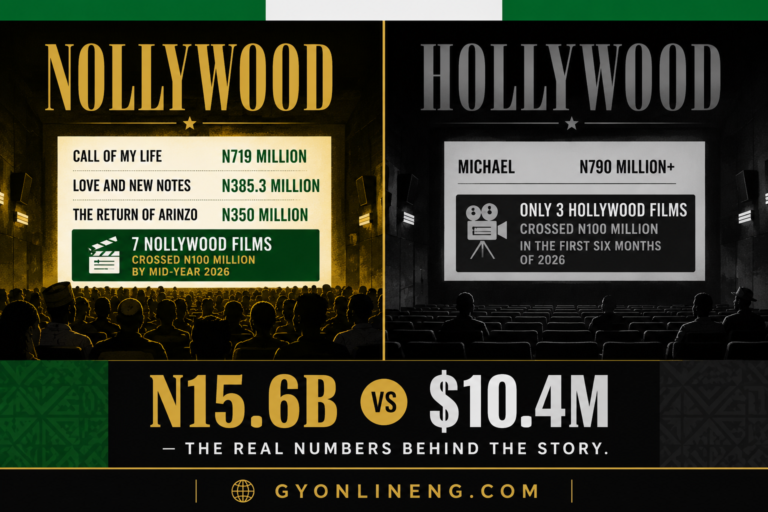

Nollywood’s box office hit N11.5 billion in 2024, surging to N11.3 billion by October 2025 alone, driven by cinema releases that drew local audiences back to theaters. In 2025, Nigeria’s cinema sector recorded between N15.6 billion and N20 billion in regional box office revenue, with Nollywood titles now accounting for nearly half of total box office takings their strongest-ever share.

This is not a coincidence. The withdrawal of subscription streaming money forced Nigerian filmmakers to rebuild their relationship with the domestic theatrical audience. Films that had been shaped by Netflix’s preference for “casual viewing” categories, faster pacing, immediate emotional hooks, content designed for distracted viewers on a couch: started giving way to films built for the communal cinema experience.

Funke Akindele, Toyin Abraham and Mo Abudu focused on big-screen cinema releases that capitalised on local hype. Everybody Loves Jenifa generated N2.8 billion, Oversabi Aunty by Toyin Abraham generate N1.6 billion. Behind The Scenes led theatrical charts. The strategy that had worked before Netflix arrived build for the Nigerian audience first, let international distribution follow proved to work again when the international money left.

The box office surge and the YouTube revenue are the same structural argument made from two different angles. Nigerian audiences will pay for Nigerian content that speaks to them. They will fill cinemas for it. They will watch it on YouTube in their tens of millions. What they will not do, in meaningful numbers, is subscribe to a foreign-owned platform at a price point calibrated for a different economy to access it.

The Trap Nollywood Must Not Fall Into

The YouTube model has a specific structural weakness that the industry needs to name clearly.

YouTube’s Partner Program thrives on volume. Some Nigerian producers now release films directly to YouTube, reaching millions easily. This empowers the filmmaker with instant global distribution but also allows Google to harvest massive amounts of advertising revenue and user data from a demographic that was previously off the grid.

The parallel to the Nigerian music streaming situation is exact. Nigerian artists generate 30.3 billion Spotify streams and receive N60 billion — which in dollar terms has been flat for three years because the naira keeps losing value while Google and Spotify capture the real dollar growth in advertising and subscription revenue. Nigerian filmmakers are generating $120 to $200 million annually in YouTube advertising revenue. How much of that is going to Google? All of it minus the creator’s share. Who controls the creator’s share calculation? Google does.

Nollywood traded dependence on Netflix’s commissioning decisions for dependence on YouTube’s algorithm and advertising rate calculations. Both are foreign platforms whose revenue optimisation serves shareholders in California, not filmmakers in Lagos.

The sustainable version of what Nollywood needs is not subscription streaming at unaffordable prices and not YouTube revenue sharing on terms set by Google. It is a domestic distribution infrastructure that captures the value of Nigerian film content within a Nigerian economic framework — whether that is through strengthened theatrical networks, genuinely competitive local streaming products, or hybrid models that use YouTube as a reach mechanism while building owned audience relationships around it.

New platforms like Kava are attempting to reshape African streaming with different models. Whether any of them can build what Showmax could not, a subscription product that works at Nigerian economic realities — remains the industry’s open question.

What Comes Next for Nollywood Streaming Economy

The Nollywood money picture in 2026 is better than it looks from the outside and more structurally precarious than the box office numbers suggest.

YouTube is generating real revenue at real scale. The theatrical market is growing at its fastest rate in years. The international licensing market, while reduced, still exists for premium projects. The industry that produces 2,500 films a year has found multiple revenue streams and is using all of them simultaneously.

What it has not built is a distribution infrastructure that captures value domestically and keeps it domestic. Every major revenue stream flows through a foreign platform at some point — YouTube, Spotify, Netflix licensing, Amazon Prime licensing. The Alaba International Market parallel that applies to Nigerian music applies equally to Nigerian film. The content is Nigerian. The distribution infrastructure is not. And until that changes, the growth in box office revenue and YouTube earnings will continue to benefit Nigerian creators less than it benefits the platforms that carry the content to its audience.

Nollywood did not collapse when Netflix left. That resilience is real. The question now is whether the industry uses the space that the subscription model’s failure created to build something that belongs to it.