Here is a number that does not appear in any of the Afrobeats decade celebrations for Nigerian music industry.

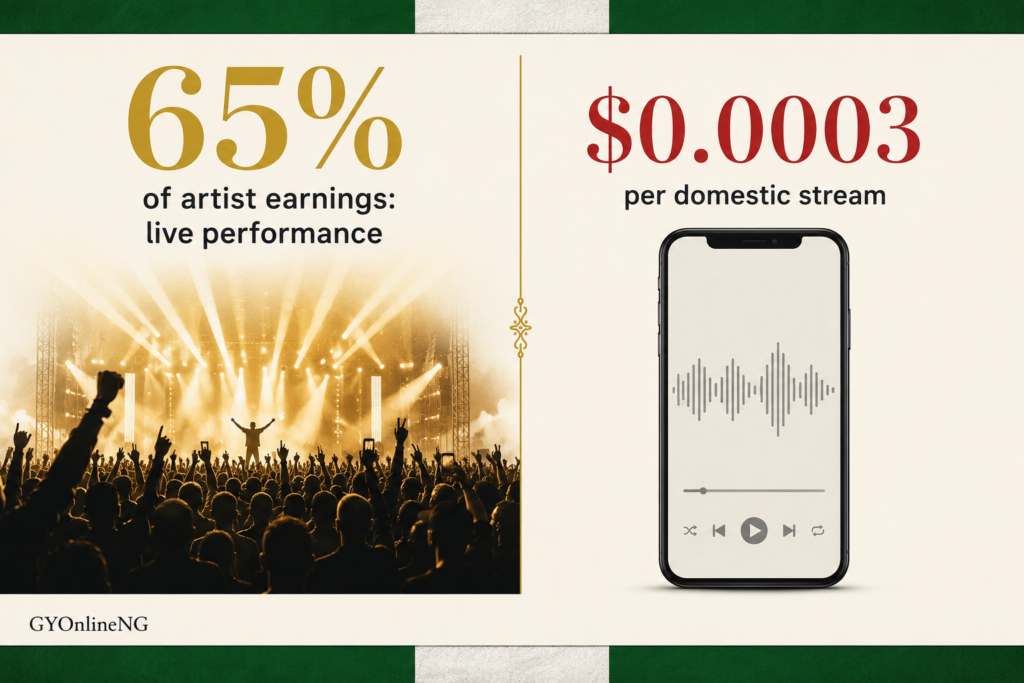

Live performances and touring account for between 65.7 and 74 percent of total artist earnings in the Nigerian music industry. Streaming the metric the entire global conversation uses to measure Afrobeats’ success accounts for roughly 30 percent of what Nigerian artists actually earn.

That gap is not a bug. It is the most precise description of what Nigerian music’s structural problem actually looks like. The industry generates its cultural credibility through streaming. It generates most of its money through live performance. And the live performance economy: the venues, the ticketing infrastructure, the touring logistics, the booking ecosystem is almost entirely underdeveloped relative to the streaming numbers that represent it to the world.

What the Per-Stream Rate Actually Tells You

One million streams from Nigerian listeners generate approximately $300 in royalties for a Nigerian artist. The same one million streams originating from Sweden generate up to $10,000. That is a difference of more than 3,200 percent from the same number of plays of the same song.

The reason is not mysterious. Nigeria’s Spotify Premium plan costs approximately N1,300 per month, roughly $0.82 at mid-2025 exchange rates. A US subscriber pays $11.99. Spotify’s royalty pool in each market is proportional to the subscription revenue generated there. More subscribers paying higher prices means more money in the pool. More money in the pool means more per stream for every artist whose music gets played from that market.

Nigerian artists in 2025 accumulated 30.3 billion streams domestically. Local consumption of Nigerian music on Spotify jumped 170 percent year on year. More Nigerians than ever are listening to more Nigerian music. The per-stream rate they generate is $0.0003. The naira’s depreciation compounds the problem in 2021 a N900 Spotify subscription was worth about $2.50. By 2025, N1,300 converted to only $0.82. Nigerian fans are technically paying more in naira every year. Artists are earning less in dollars every year.

This is why the N60 billion headline figure from Spotify’s Loud and Clear report obscures more than it reveals. In dollar terms, Nigerian artist earnings from Spotify have been approximately flat for three consecutive years. The naira growth looks impressive. The dollar plateau is the actual economic reality.

Who Controls the Pipes

In 2025, three foreign companies controlled 68 percent of Nigerian music streaming distribution. EMPIRE led with the largest market share, boosted by Asake before his exit to Giran Republic and other major signings. Universal Music Group came second at approximately 21 percent market share through Mavin-affiliated releases from Rema and Ayra Starr. Sony Music trailed third at 14 percent, carried largely by Tems and Shallipopi through the Since ’93 subsidiary label. Wizkid‘s long-form Afrobeats output remained the most streamed catalogue across all three distributors.

Three California-headquartered companies control 68 percent of the distribution of Nigerian music. That figure tells you something the streaming charts do not.

Nigerian music exports cultural influence at a scale that most countries never achieve. The infrastructure that converts that cultural influence into financial value is owned almost entirely by foreign entities. Universal, Sony and EMPIRE capture distribution margins on every Nigerian stream globally. Spotify captures subscription revenue and advertising revenue from every Nigerian listener. YouTube captures advertising revenue on every Nigerian music video view. The artist receives a royalty calculated by systems they do not control, distributed through infrastructure they do not own, at rates determined by market conditions they cannot change.

A KPMG report identified the specific reason foreign distributors filled this vacuum the Nigerian music industry has struggled with a vaguely defined business structure, with a lack of formal auditing and corporate governance making local labels appear difficult and confusing for traditional investors. The infrastructure gap was not filled by foreign companies because Nigerian companies were absent. It was filled because Nigerian companies were structured in ways that made them invisible to capital.

What Live Music Reveals That Streaming Conceals

The live performance data is the most honest mirror the Nigerian music industry has.

Licensing for live events in Nigeria remains a documented nightmare of multiple taxation and extortion. There is no national music policy worth the name. There is no meaningful government investment in venues or training. Ticket prices for major Lagos concerts in December 2025 priced out the very fans who built those artists on the streets. Traffic gridlock, venue power failures and last-minute cancellations frustrated even the biggest productions.

Yet live performance still accounts for 65 to 74 percent of total artist earnings. That figure is not a sign of a thriving live music economy. It is a sign that streaming pays so little relative to what the cultural footprint deserves that live performance — despite all its infrastructural failures — still pays more.

Burna Boy performing to 80,000 people at Crystal Palace in London generates more revenue in one night than multiple shows in Lagos at equivalent capacity would generate in a week. This is not because Nigerian fans value the music less. It is because venue infrastructure in Nigeria cannot yet capture value at the scale the music demands. The ticketing systems are inadequate. The security infrastructure is unreliable. The transport access to venues is chaotic. The sponsorship market for live events is under-developed relative to what exists in London or New York.

Artists who can access international touring circuits are doing so partly because of the cultural moment but also because the domestic live music infrastructure cannot yet monetise their audience at the level their streaming numbers justify. Davido’s 5ive Alive Tour covering 31 cities across 12 countries on four continents is an extraordinary commercial achievement. It is also a structural statement about where the money is relative to where the audience is.

The Distribution Trap Nollywood Also Fell Into

The parallels between what is happening in Nigerian music and what happened in Nollywood with streaming are not coincidental. They are the same structural problem expressed in two different creative industries.

Nollywood generated an estimated $120 to $200 million annually through YouTube advertising while subscription platforms burned through hundreds of millions of dollars failing to find a viable model in Nigeria. The YouTube revenue is real but it flows through Google’s systems at rates Google determines, captured through infrastructure Google owns, with audience data Google holds.

Nigerian music generates N60 billion annually on Spotify while the dollar equivalent has been flat for three years. The streaming revenue is real but it flows through Spotify’s systems at rates Spotify determines, captured through infrastructure EMPIRE and Universal and Sony distribute, with audience data platforms hold.

Both industries are producing content that billions of people want. Neither industry has built the domestic infrastructure to capture the full value of that demand in a way that keeps the money in Nigerian hands.

The Alaba International Market parallel applies directly. For two decades, Nigerian music moved through Alaba’s distribution network — traders who pressed, duplicated and circulated cassettes and CDs across Nigeria and the diaspora. Artists depended on Alaba to reach their audience while Alaba captured the distribution margin and piracy eroded whatever remained. The system worked for distribution. It did not work for artist economics.

The current structure has changed the technology of distribution without changing its economics. Spotify replaced Alaba as the distribution infrastructure. EMPIRE and Universal replaced the Alaba traders as the intermediaries. The cultural product is Nigerian. The infrastructure that monetises it is not.

What Building at Home Actually Requires

The Creative and Tourism Infrastructure Corporation established in late 2024 and developed through 2025 represents the first serious government acknowledgment that creative industry infrastructure is an economic policy matter. The projection of the creative economy as a $7.23 trillion contributor to national GDP is a political statement as much as an economic one. Whether it produces concrete investment in the specific infrastructure gaps that matter — venue development, royalty collection systems, streaming platform technology, music education — is the question that 2026 and 2027 will answer.

The Tiwa Savage Foundation‘s partnership with Berklee College of Music addressed the training pipeline. The 18 scholars who received full three-year Berklee scholarships at the National Theatre in April 2026 will become the music lawyers, publishers, A&R professionals and music technology builders that the industry’s next phase requires. That is a 2028 and 2029 solution. It is the right long-term investment. It does not solve the 2026 structural problem.

The 2026 structural problem requires three things that are available to the industry right now without waiting for government policy or institutional development.

First, transparent royalty accounting. The KPMG finding about vaguely defined business structures and lack of formal auditing is not a reflection of Nigerian creative limitations. It is a reflection of governance choices that can be changed. Labels and distributors that open their books to independent audit build the credibility that attracts domestic and international capital on terms the industry controls rather than terms foreign distributors dictate.

Second, collective bargaining infrastructure. Nigerian artists negotiate individually with platforms and distributors whose legal teams have decades of contract experience. An industry association with genuine legal capacity — not a ceremonial body but one that negotiates streaming rates, distribution terms and licensing structures on behalf of its members — would change the terms on which Nigerian music enters foreign distribution systems.

Third, domestic concert infrastructure investment. The venue problem and the ticketing problem and the security problem and the transport problem are solvable. They are expensive to solve and the returns are long-term. But the industry generates enough revenue in international touring to fund domestic venue development if that revenue were directed toward it rather than lifestyle and international property.

The Honest Position

Nigerian music is genuinely global in a way it has never been before. The streaming numbers are real. The international touring revenue is real. The cultural influence is real and it is not going away.

What is also real is that the industry has spent a decade building global reach without building domestic infrastructure. The streaming rates are low because the domestic subscription market is priced for Nigerian economic reality. The live performance economy is underdeveloped because venue infrastructure requires capital the industry has not committed. The distribution margin flows to foreign companies because Nigerian companies have not built the governance structures that attract competitive investment.

None of this is solved by the next viral single or the next Coachella booking. Those things are real achievements. They do not change the underlying economics.

The next phase of Nigerian music is a domestic infrastructure project disguised as a cultural moment. The artists who understand that and invest accordingly — in ownership, in domestic audience monetisation, in the legal and financial systems that make their catalogues defensible — will be the ones who are still building careers when the current streaming wave plateaus further.

The ones who do not will find that the global moment was real and the money from it was largely captured by someone else.

Sixty billion naira sounds like a lot. Three consecutive years of the same number in dollars is the whole story.